Affiliate disclosure: This blog post contains affiliate links. If you click on a link and make a purchase, I may receive a small commission at no extra cost to you. I only recommend products I truly believe in and have used personally. Your support helps keep this blog running and allows me to continue providing valuable content. Thank you for your support!

Dave Ramsey’s Baby Steps have helped millions of people escape debt and build wealth. His straightforward approach offers a clear roadmap when you’re drowning in financial chaos.

But after working with countless people struggling with debt over my 17 years in banking, I’ve learned that while the Baby Steps are powerful, they don’t work the same way for everyone.

If you’re considering following Dave Ramsey’s program, you need to know what really happens when real people try to implement these steps.

Let me share what I’ve discovered works beautifully, what needs modification, and how to make the Baby Steps work for your unique situation.

Understanding Dave Ramsey’s 7 Baby Steps

Before diving into real-world applications, let’s review the complete Baby Steps system:

Baby Step 1: Save $1,000 for a starter emergency fund.

Baby Step 2: Pay off all debt except your mortgage using the debt snowball.

Baby Step 3: Build a full emergency fund of 3-6 months of expenses.

Baby Step 4: Invest 15% of your income for retirement.

Baby Step 5: Save for your children’s college fund.

Baby Step 6: Pay off your mortgage early.

Baby Step 7: Build wealth and give generously.

The beauty of this system lies in its simplicity and psychological approach. Rather than trying to do everything at once, you focus intensely on one step at a time.

What Works Brilliantly: The Psychology Behind the Steps

The $1,000 Emergency Fund Creates Real Peace of Mind

I’ve seen people’s entire demeanor change after saving their first $1,000. It’s not about the money itself, it’s about proving to yourself that you can take control. This small buffer prevents you from adding new debt when minor emergencies arise.

However, if you’re living paycheck to paycheck, $1,000 might feel impossible. Start with $100 or even $50.

The psychological victory of reaching your first goal matters more than the exact amount.

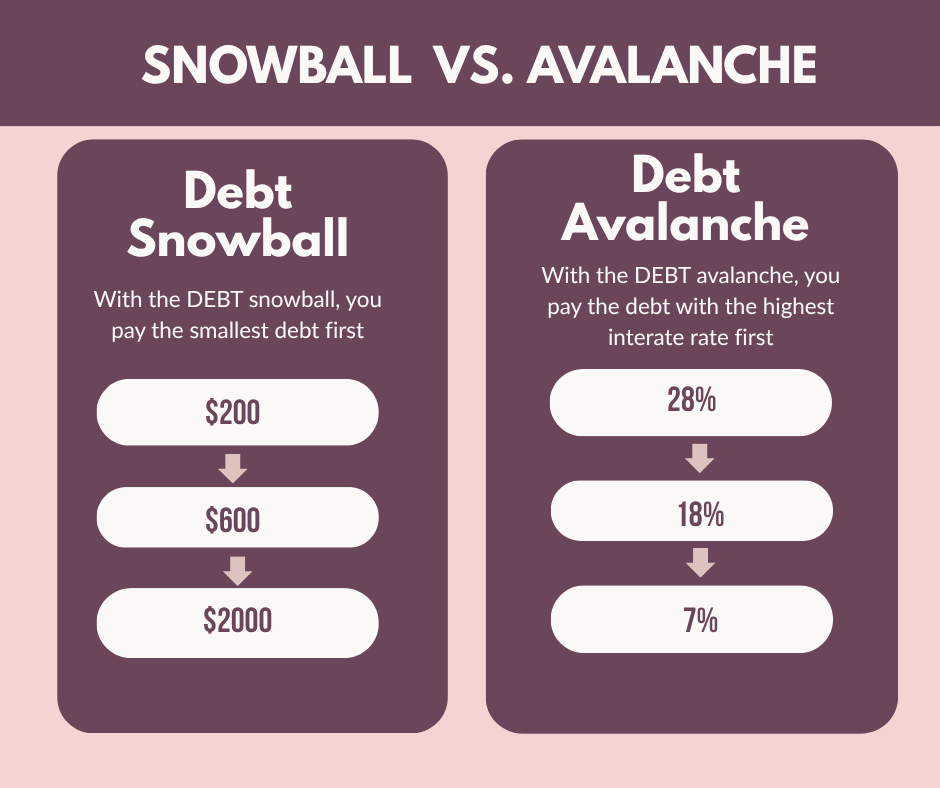

The Debt Snowball Actually Works Better Than Math Says It Should.

Dave Ramsey advocates paying off your smallest debts first, regardless of interest rates. Mathematically, the debt avalanche method (highest interest first) saves more money.

But I’ve watched people stick with the snowball method when they would have quit the avalanche approach.

The quick wins from eliminating small debts create momentum that keeps you motivated through the harder months.

When you’re broke and overwhelmed, motivation trumps mathematics every time.

Where the Baby Steps Need Real-World Adjustments

Baby Step 1 Can Take Forever If You’re Truly Broke.

If you’re barely covering basic expenses, saving $1,000 might take six months or longer. During this time, you’re supposed to only make minimum payments on debt, which means your balances keep growing due to interest.

My modification: If saving $1,000 takes more than three months, start with a smaller emergency fund ($250-500) and move to Baby Step 2. You can build the full $1,000 while paying off debt.

The Debt Snowball Ignores Some Harsh Realities

Dave’s approach assumes you can make minimum payments on all debts while attacking one aggressively. But what if you can’t even afford minimums? What if some debts are in collections while others aren’t?

My modification: Prioritize debts that affect your housing, transportation, and essential services first, regardless of balance size. You can’t follow any debt plan if you’re homeless or can’t get to work.

Baby Step 3 Might Be Too Conservative for Some

Building 3-6 months of expenses before investing means potentially years without retirement contributions. If your employer offers 401(k) matching, you’re leaving free money on the table.

My modification: If your employer offers matching, contribute enough to get the full match starting in Baby Step 2, but don’t increase contributions until Baby Step 4.

Making the Baby Steps Work When You’re Broke.

Start Where You Are, Not Where You Think You Should Be

The Baby Steps assume you have some financial stability. If you’re choosing between rent and groceries, you need to stabilize your situation first before following any structured plan.

Focus on covering your four walls first: housing, utilities, food, and transportation. Only after these are secure should you begin Baby Step 1.

Increase Income Aggressively During Baby Steps 1 and 2

Dave emphasizes cutting expenses, but when you’re broke, there might not be much left to cut. Instead, focus intensely on increasing income through side jobs, overtime, creating digital income, or selling possessions.

Every extra dollar you earn during the early steps accelerates your progress exponentially. An additional $200 monthly can turn a two-year debt payoff into a one-year journey.

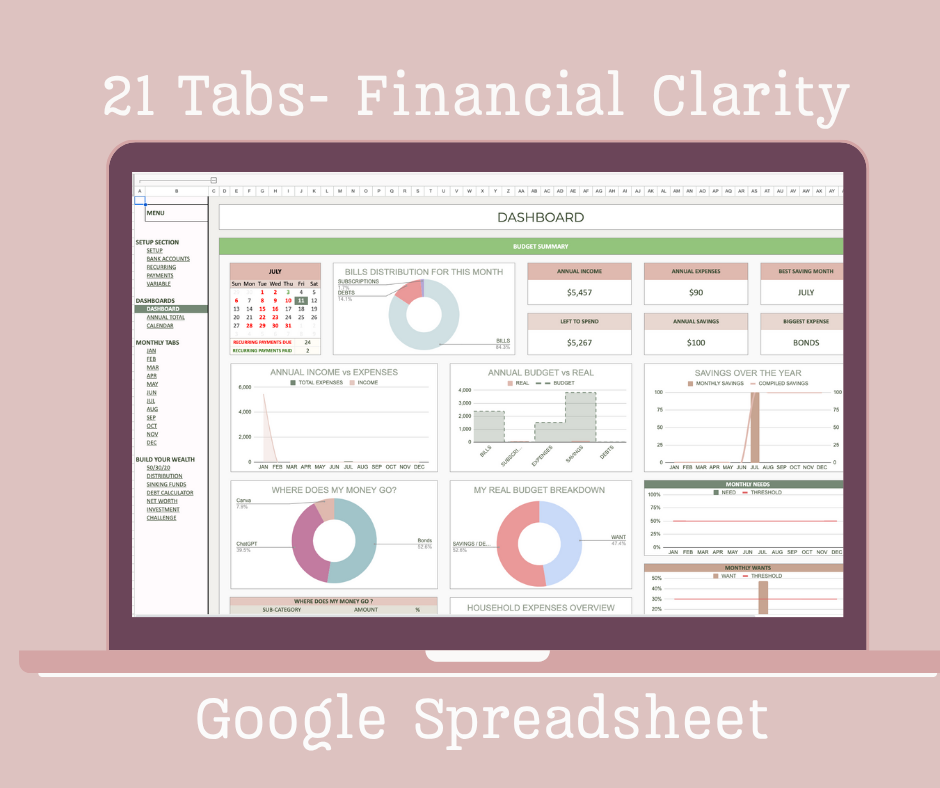

Use Technology to Your Advantage

Dave’s program was designed before smartphones and apps made money management easier. Use technology to automate what you can and track progress in real time.

Consider using a comprehensive budgeting system like my Financial Clarity Google Spreadsheet for $27 to track your Baby Steps progress and find money you might be missing.

The Baby Steps vs. Real Life: Common Challenges

When Emergencies Happen During Baby Step 2.

You’re making progress paying off debt when your car breaks down. Do you use credit cards or pause debt payments to rebuild your emergency fund?

My approach: Use the emergency fund, then pause extra debt payments temporarily while you rebuild it to $1,000. This prevents new debt while maintaining your safety net.

When Your Income Is Irregular

The Baby Steps work best with steady income, but many people have irregular paychecks from commission jobs, seasonal work, or freelancing.

My modification: Base your emergency fund on your lowest income months, not your average. You need more cushion when income fluctuates unpredictably.

Beyond the Baby Steps: What Comes Next

The Real Test Comes After Debt Freedom

Getting out of debt is actually easier than staying out of debt. The Baby Steps give you a clear target and deadline. Building wealth requires different skills and mindset shifts.

Baby Steps 4-7 require you to think long-term and resist lifestyle inflation as your income grows. This is where many people struggle after successfully completing the first three steps.

Building Wealth Habits During Debt Payoff

Don’t wait until Baby Step 4 to develop wealth-building habits. Start reading about investing, learning about compound interest, and understanding how wealthy people think. The knowledge you gain during debt payoff will serve you well in wealth building.

Is Dave Ramsey’s Plan Right for You?

The Baby Steps work exceptionally well for people who:

- Need structure and clear guidelines

- Respond well to psychological motivation

- Have stable income and employment

- Want a proven system they don’t have to customize

The Baby Steps might need modification if you:

- Have irregular income or are underemployed

- Face housing instability or other basic needs issues

- Have complex debt situations (student loans, business debt, tax debt)

- Are naturally motivated by mathematical optimization

Your Next Steps to Financial Freedom

Whether you follow Dave Ramsey’s Baby Steps exactly or adapt them to your situation, the key is starting where you are and taking consistent action. The perfect plan you never start won’t help you, an imperfect plan you actually follow will transform your life.

Remember, personal finance is exactly that; personal. Use the Baby Steps as your foundation, but don’t be afraid to make adjustments that fit your unique circumstances.

Ready to dive deeper into practical debt elimination strategies? Check out my comprehensive blog on “How to Pay Off Debts Quickly Even When You’re Broke” for specific tactics that work when traditional advice isn’t enough.

The path to financial freedom isn’t always linear, but it’s always possible. Your journey starts with the first step you take today.